Why You Should Never Accept the First Insurance Offer

Following a serious accident, a quick settlement offer from an insurance adjuster can feel like a relief. However, this speed is a calculated tactic. Insurance companies often offer a fraction of a claim’s true value before the victim even knows the full extent of their injuries. At Murphy, Falcon & Murphy, we have spent decades protecting clients from these “low-ball” traps. Accepting that first check is a permanent decision.

The Trap of the “Final Release”

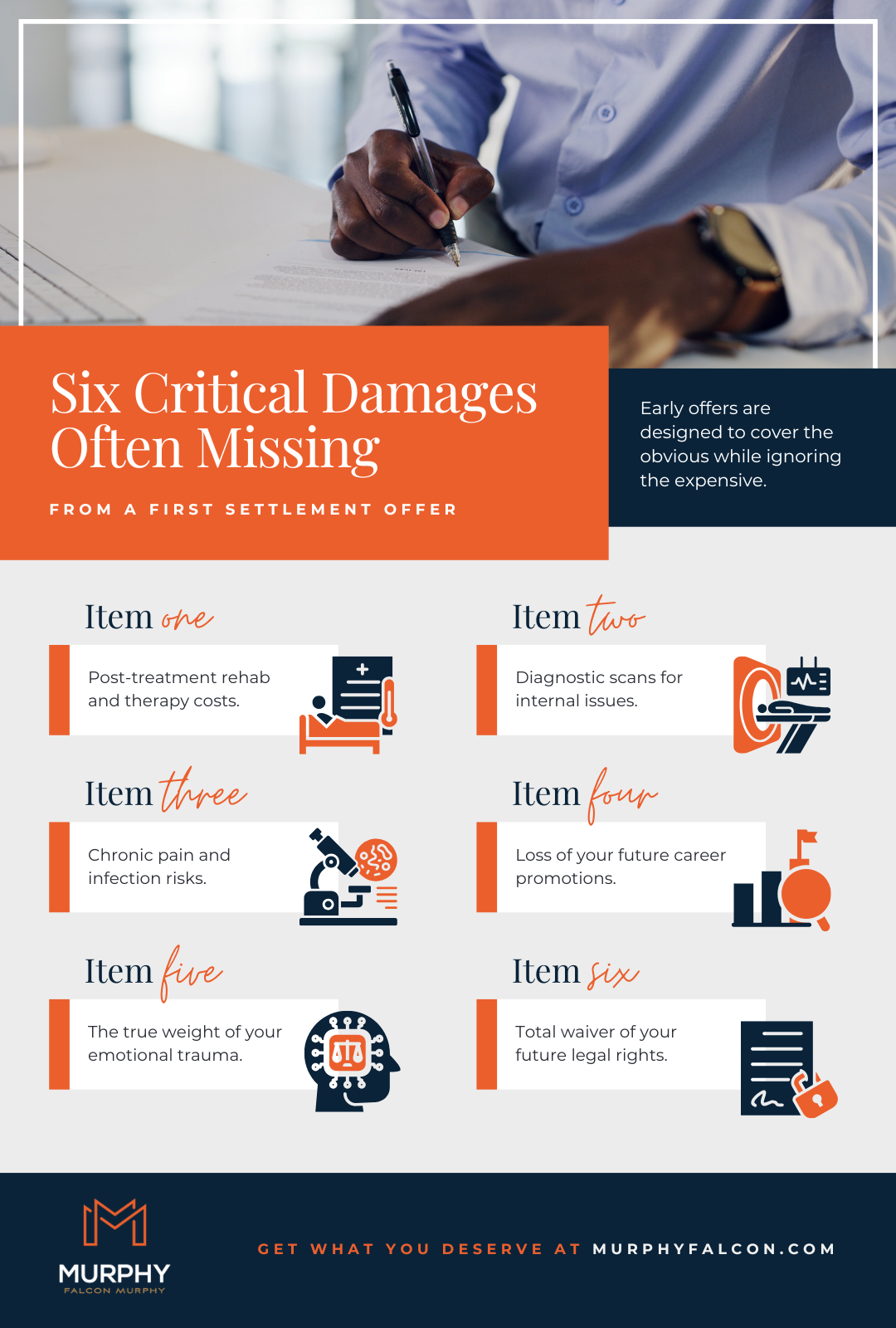

The most dangerous part of a first insurance offer isn’t the low dollar amount—it’s the paperwork. By cashing that check, you almost always sign a “Final Release of Liability.” This document waives your right to ever seek more money for that specific accident. If you discover months from now that you need a spinal fusion or chronic pain prevents you from working, you cannot go back. You are effectively locked out.

Underestimating Future Medical Needs

Insurance adjusters are not doctors. Their valuation of your case is based on a spreadsheet, not your long-term health. Many injuries, particularly those involving the brain or spine, do not reveal their full severity for weeks. If you settle within the first 30 days, you are essentially gambling that you won’t need future surgery or therapy. We ensure that your claim accounts for the point where doctors know exactly what your future looks like.

Ignoring Diminished Earning Capacity

A serious injury doesn’t just cost you the time you’ve already missed from work; it can alter your entire career. If you can no longer stand for eight hours or focus for long periods, your lifetime earning potential has been slashed. The insurance company’s first offer will rarely account for the loss of future promotions or retirement contributions. We use vocational experts to prove exactly what that loss is worth over your career.

The Psychological Toll and Intangible Losses

How do you put a price on the inability to pick up your child or the constant anxiety following a traumatic wreck? Maryland law allows for noneconomic damages, commonly known as pain and suffering. Insurance companies notoriously undervalue these losses because they are subjective and harder to quantify. However, we know these are the most real parts of your injury. We use a trial-ready approach to force adjusters to recognize the human cost involved.

The Power of Trial-Ready Advocacy

Insurance companies track which law firms settle quickly and which ones go to court. If you hire a “settlement mill” firm, the adjuster has no incentive to offer a fair amount because they don’t fear a trial. When Murphy, Falcon & Murphy takes your case, the dynamic shifts. They know we have the resources and the reputation to take a case to a jury verdict. That threat finally moves a low-ball offer.

The insurance company’s goal is to close your file as cheaply as possible. Our goal is to ensure you have the resources to rebuild. Before you sign anything or give a recorded statement, you need professional legal advice. If you or a loved one has been injured due to someone else’s negligence, call a lawyer at Murphy, Falcon & Murphy today to protect your rights.